Why We Invested in Clover Health

PUBLISHED BY Abhas Gupta

SOURCE Medium

April 11, 2016

As early stage venture investors who only invest in a select number of companies annually, we unfortunately have to pass on many great entrepreneurs and compelling visions. So when we do make an investment — Clover Health’s Series B, in this case — we are inevitably asked, “Why them? What’s special about that company?”

I hope this post sheds light on why we believe Clover Health is one of the most exciting companies in both digital health and insurance — two sectors that are key areas of investment focus for us at Wildcat Venture Partners. Below, I elaborate on our rationale along each of the three core factors that underlie all our investment decisions: the market, the team, and the team’s unique insight.

THE MARKET

As far back as 2011, it was clear to us that the the shift to value-based care was going to unlock a trillion-dollar opportunity in healthcare. This has been the crux of our digital health investment thesis: we actively seek out scalable, technology-driven companies who either take on risk themselves or enable risk-bearing entities.

Clover Health operates in the Medicare Advantage market where private organizations take on the full-capitated risk of Medicare patients, so it fit squarely within our investment thesis. Additionally, we were attracted to the sheer magnitude of the opportunity: each Medicare patient represents $10K of premium revenue and thus every county that Clover enters is a $100M revenue opportunity — a figure so staggering that it has few parallels today (e.g., Apple, Exxon, AT&T, Verizon).

THE TEAM

From the first time we met Vivek Garipalli and Kris Gale last summer, we were instantly enamored with their backgrounds and vision for the company. Pursuing this opportunity requires a team with strong domain expertise — understanding of market dynamics, provider relationships, the revenue chain, compliance requirements, reserve needs, etc. — and seasoned technical leadership to rapidly execute on the sprawling technology stack. With Vivek’s experience turning around health systems and Kris’s experience managing large engineering teams, we were confident that in a market where there is little margin for error (literally and figuratively), this would be a team that could define the strategy, recruit the talent, and ultimately execute on the vision.

THE INSIGHT

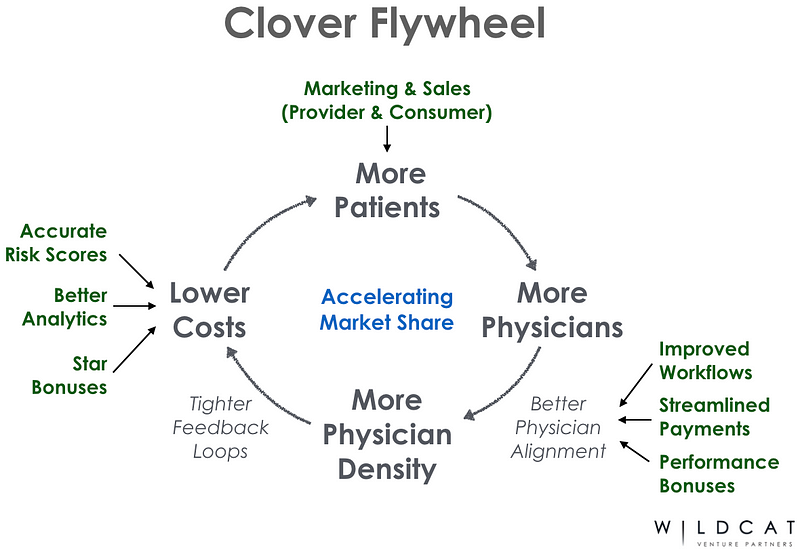

Clover’s mission is to bring the outcomes and cost efficiency of Kaiser Permanente’s integrated health system to the rest of the country. Vivek and Kris’s elegant insight is to achieve this mission through technology and light services, thereby avoiding the onerous and capital intensive process of acquiring the underlying hospitals or directly employing all the physicians. Though it is significantly more nuanced, their core insight is captured by the Clover Flywheel, illustrated below:

The Clover Flywheel is a powerful, self-reinforcing, multi-staged network effect whose end result is accelerating market share capture. Its key components are described below at a high-level:

Lower Costs — by integrating data, applying analytics, and optimally deploying care teams, Clover is able to improve patient outcomes and avoid costly hospital admissions; these savings, coupled with Medicare bonuses for better quality care, ultimately result in lower costs for consumers.

More Patients — effective marketing and sales that highlight Clover’s benefits, particularly lower costs and better outcomes, lead to more participants joining Clover’s plans.

More Physicians — new patients to Clover’s plans also bring with them more physicians, who are subsequently added to Clover’s network; through better alignment with physicians in the form of improved workflows (i.e., fewer prior authorizations, simpler scheduling, etc.), streamlined payments (improving revenue cycle management), and higher performance bonuses, Clover can expect both physicians and patients to have a more favorable overall experience.

More Physician Density — better physician alignment and user experiences inevitably lead to Clover covering an increasing share of practices’ patient population; as a result, Clover’s light services/care teams can more effectively engage and coordinate with these physician practices, further improving patient outcomes. These improvements lead to even lowers costs, which then recycles through the flywheel, albeit with increasing momentum.

A critical feature of Clover’s model, and what differentiates it from other health insurance startups, is that it is not beholden to provider contracting leverage — the root, economies-of-scale competitive advantage of today’s large payers. In our view, this is a necessary prerequisite of nascent insurance startups who are competing against large, established players; otherwise, startups are essentially Davids playing at Goliath’s game (and burning through lots of venture dollars along the way).

SUMMARY

From an investment perspective, it is rare to find a true flywheel — not simply weak network effects — in any company; the ones who get it right can grow to achieve spectacular market capitalizations (e.g., Amazon, Apple, Google).

Stepping back from the machinations of the investment decision, I find it deeply rewarding to work with such innovative and visionary entrepreneurs. Clover has the potential to realign the healthcare system in a way that is a win-win-win for patients, physicians, and Medicare; it is incredibly exciting to be a part of that mission, the impact of which cannot be understated.